Key Findings

- Exempting groceries from the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. base reduces economic efficiency without achieving its objective of enhancing taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. progressivity.

- The poorest decile of households experiences 9 percent more sales tax liability with a grocery tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. than they would if groceries were taxed and the general rate were reduced commensurately.

- Grocery tax credits provide actual progressivity at a lower cost than the broad exemption of groceries. Under a revenue-neutral expansion paired with a $75 per person credit, the poorest decile of households would save 31 percent on sales tax liability.

- Sales taxes are more stable and pro-growth than many other forms of taxation, especially income taxes, so policymakers have an opportunity to increase tax progressivity, enhance revenue stability, and improve economic competitiveness by taxing groceries, providing a credit, and using the remaining revenue from base broadeningBase broadening is the expansion of the amount of economic activity subject to tax, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. Narrow tax bases are non-neutral, favoring one product or industry over another, and can undermine revenue stability. to cut income taxes.

Introduction

It is commonly assumed that the exemption of groceries from state sales tax bases has a progressive effect, with a distribution of benefits which favors low- and middle-income taxpayers. It is primarily upon this basis that lawmakers in most states have carved groceries out of the sales tax base. The assumption is simple and, on the surface, reasonable—and it is wrong. As counterintuitive as it may seem, the lowest decile of households experiences 9 percent more sales tax liability under a sales tax with a grocery exemption than one with groceries in the base, assuming that rates are adjusted to generate the same amount of revenue from each tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. .

Seven states tax groceries at the ordinary state sales tax rate, and another six tax them at reduced rates. Recent years have seen efforts to reduce or repeal the sales taxation of groceries in more than half of these states, however, with policymakers from both parties championing the exemption as a means of enhancing sales tax fairness.

The idea that a grocery exemption creates a more equitable sales tax base often goes unquestioned, leaving policymakers only to grapple with the trade-off between equity and efficiency. But the assumption is unwarranted. Grocery exemptions are a middle-income, not a low-income, benefit—and middle earners can be more efficiently made whole through grocery tax credits. The distributional effects of grocery taxation diverge sharply from most policymakers’ expectations, which has dramatic ramifications for this ongoing debate and suggests better ways to achieve policymakers’ desired aims. Policymakers might be far less eager to further carve up the sales tax base if the actual incidence of the policy were better appreciated.

State Taxation of Groceries

In states which exempt groceries from the sales tax base, the notion that some states still tax them is often regarded as curious or even anachronistic. Proposals to restore groceries to sales tax bases from which they have been previously exempted tend to be met with substantial resistance. This may be particularly true if groceries represent the lion’s share of a planned base-broadening effort, as was the case with a quickly rescinded policy adopted in Utah but not implemented in the face of public opposition. Yet 13 states do tax groceries to some degree, typically with a minimum of public discontent. What’s more, they may represent the minority of states, but the economic evidence strongly suggests that they are in the right.

Of these 13 states, only three tax groceries at the ordinary rate without providing some sort of offsetting grocery tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. . Alabama, Mississippi, and South Dakota treat groceries no differently than other forms of taxable consumption. Hawaii, Idaho, Kansas, and Oklahoma tax groceries at the ordinary rate but provide a credit or rebate to lower-income households intended to offset this tax liability. Finally, Arkansas, Illinois, Missouri, Tennessee, Utah, and Virginia tax groceries at a reduced rate (with Utah recently adopting a credit to go along with the reduced rate).[1]

| State | Ordinary Rate | Grocery Rate | Targeted Offset |

|---|---|---|---|

| Alabama | 4.00% | 4.00% | |

| Arkansas | 6.50% | 0.125% | |

| Hawaii | 4.00% | 4.00% | ✓ |

| Idaho | 6.00% | 6.00% | ✓ |

| Illinois | 6.25% | 1.00% | |

| Kansas | 6.50% | 6.50% | ✓ |

| Mississippi | 7.00% | 7.00% | |

| Missouri | 4.225% | 1.225% | |

| Oklahoma | 4.50% | 4.50% | ✓ |

| South Dakota | 4.50% | 4.50% | |

| Tennessee | 7.00% | 4.00% | |

| Utah | 4.85% | 1.75% | ✓ |

| Virginia | 5.30% | 2.50% | |

| Source: Tax Foundation, Facts & Figures 2022. | |||

State definitions of groceries vary, but mostly at the margin. All states distinguish between prepared and unprepared foods, with prepared foods subject to tax. In determining what constitutes prepared food for sales tax purposes, states take into account whether the food is sold hot, whether it is sold with utensils, whether it is combined with other foods to comprise a meal, and more. In some states, the mere availability of a microwave, napkin dispenser, condiments, and cutlery may be sufficient to turn the packaged foods with which they can be used into “prepared foods”; elsewhere, it is necessary that they be given to the purchaser. Typical examples of prepared foods regularly available in grocery stores would include rotisserie chickens, prepackaged sandwiches, any items from a hot food bar, and deli items like coleslaw or potato salad.[2]

The difficulty of defining groceries for tax purposes is often a source of humor in the dreary world of tax professionals. Wisconsin’s Department of Revenue published a rule, with 10 examples, for determining when an ice cream cake constituted taxable prepared food.[3] Iowa used to exempt pumpkins if sold for consumption but tax them if used for decorative or other non-food purposes,[4] asking way more of supermarket clerks than is reasonable. States also differ on whether soda and candy are treated as groceries for purposes of a tax exemption, and, inevitably, on how to define the terms. Frequently, the presence of flour as an ingredient is sufficient to declare an item not to be candy, meaning that some candy bars that include wafers are exempt from sales tax, while other candy bars are subject to tax. Meanwhile, some fruit juices and flavored sparkling waters are classified as sodas for tax purposes.[5]

Tax definitions of groceries, therefore, often fail to correspond with consumers’ definitions, such that many grocery items are taxed even under a grocery tax exemption.

The Logic of Grocery Tax Exemptions

It is easy to construct the basic narrative by which policymakers have assumed that a grocery tax exemption is highly progressive. Lower-income earners, by necessity, consume a greater share of their income, and thus their sales tax liability is higher as a percentage of personal income. This is particularly salient with groceries, both because they are a necessity of life and because demand for groceries cannot fully scale with income. Try as he might, a billionaire cannot consume orders of magnitude more groceries than a minimum wage employee. Consequently, the logic runs, exempting groceries disproportionately benefits lower-income earners by reducing their taxable consumption by a greater share than it is reduced for higher earners.

This narrative, however superficially compelling, is marred by several flaws. Most importantly, it either neglects or fails to appreciate the full impact of the universal policy of exempting from sales tax any purchases made using federal food-purchasing assistance programs, primarily the Supplemental Nutrition Assistance Program (SNAP), but also the more narrowly targeted Special Supplemental Nutrition Program for Women, Infants, and Children (WIC). States’ receipt of federal grants to administer these Food and Nutrition Service-funded benefits is contingent upon exempting these purchases from sales tax, and all states do so—even if groceries are otherwise in the sales tax base. This policy alone dramatically reduces taxable consumption for the lowest income deciles.

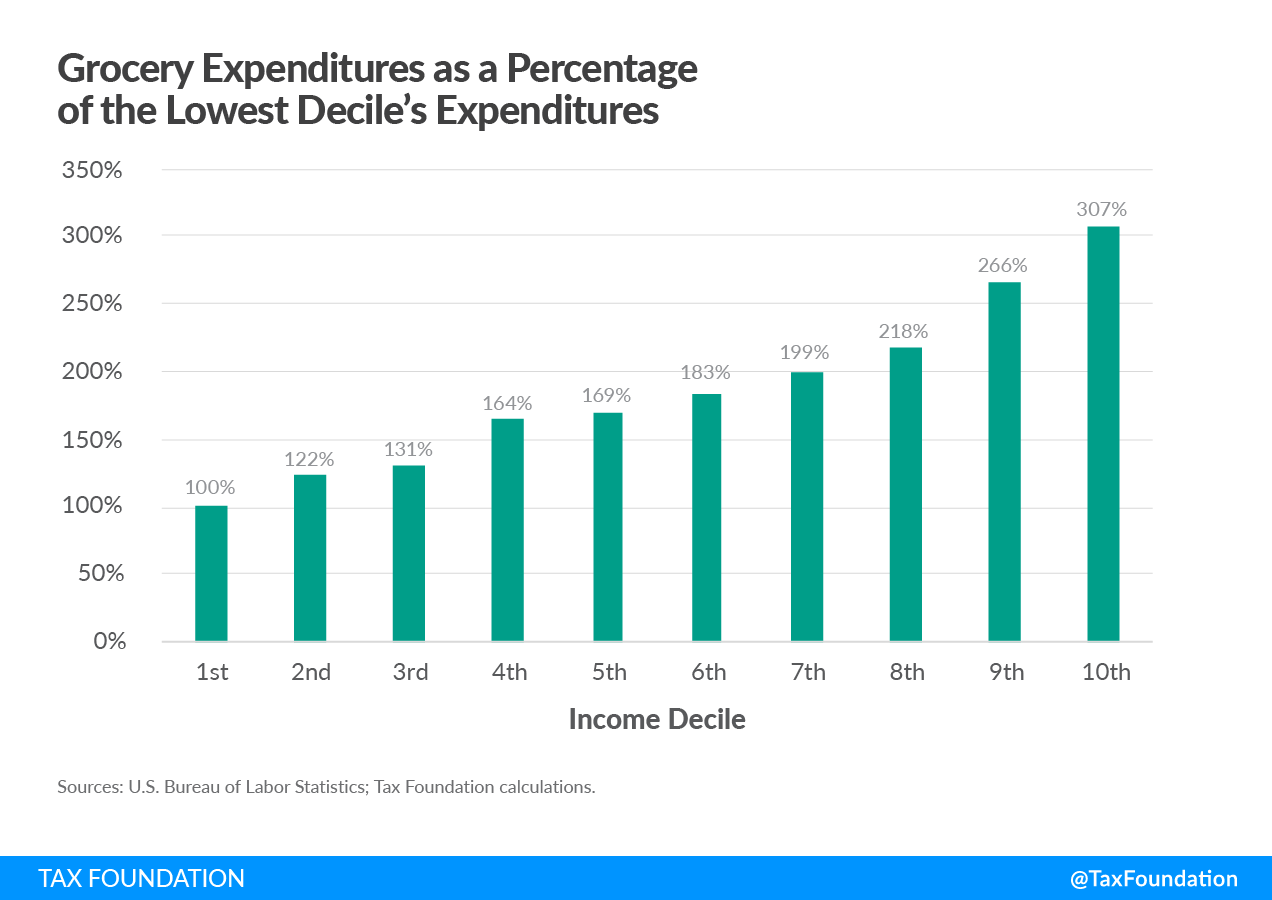

Additionally, the conventional wisdom underestimates the degree to which higher consumption of groceries does scale with income. Higher earning households purchase not only more, but higher qualities of, groceries. Low-income households, in fact, are more likely to purchase taxable substitutes to what states classify as groceries, a category that traditionally only covers unprepared foods. For lower-income working families, prepared foods—rotisserie chickens, deli items, fast food, and more—are often more economically efficient than buying raw ingredients and making home-cooked meals, but prepared foods are taxed, whereas ingredients are exempt when states adopt a grocery tax exemption. The result is that a household in the fifth decile spends almost 70 percent more than a household in the first decile, and a household in the top decile spends over three times as much as a household in the lowest.

Finally, while low-income households spend more on groceries as a share of income than do the highest-income households, they do not necessarily spend more on groceries relative to other necessities. Compositional effects matter. If lower-income families spend moderately more on groceries, as a share of income, but substantially more on other household goods, then they will be worse off under a tax code which exempts groceries but with a higher rate than would be necessary were groceries included in the base. Given not only substitution effects—prepared foods for unprepared—but also, crucially, the exemption of SNAP and WIC purchases for many low-income households, this is not just a hypothetical but the reality for many families.

The result is that a policy designed to inject progressivity into the sales tax has the opposite effect, increasing tax liability on the lowest-income households, with most savings concentrated on middle-income households that can be best helped in other ways. And once it becomes apparent that the grocery tax exemption fails to achieve its stated objective, the trade-offs associated with the policy come into sharper relief. Grocery purchases are a sizable and stable share of personal consumption, and exempting them from the primary consumption tax not only erodes the sales tax base, necessitating higher rates than would otherwise be necessary, but also increases revenue volatility.

Moreover, economists widely accept that sales taxes are more economically efficient than most other major forms of taxation, including income taxes, because they do less to influence economic decision-making and do not directly tax labor or investment. Policymakers frequently try to balance the economic efficiency of greater reliance on consumption taxation with equity concerns. Policymakers will differ on how to strike the right balance, but if the grocery tax exemption fails to address equity or equality—and even exacerbates the issue for the lowest-income households—then the efficiency losses from carving out the sales tax base come into particularly stark relief.

Our findings also cast new light on the distributional effects of grocery tax credits. These credits, under which states retain groceries in the sales tax base but provide targeted tax refunds to low-income households to defray the sales tax on food purchases, are already part of the policy toolkit, favored by many for their superior targeting but sometimes critiqued as not reaching all eligible households. Given our findings that a revenue-neutral expansion of the sales tax base to groceries already benefits the lowest decile, concerns about getting the credits to all eligible households—which are legitimate and merit further policy innovation—become less salient, as the credit enhances an increase in progressivity for the lowest-earner households, rather than offsetting it. At the same time, however, we find that the size of credit necessary to benefit the middle deciles, while not excessive, is enough to blunt a sizable portion of the sales tax rate relief that could otherwise be made possible by including groceries in the sales tax base.

Distributional Effects of a Grocery Tax Exemption

For purposes of this analysis, we constructed a representative sales tax base that includes most final consumption of consumer goods but relatively few consumer services.[6] Then, using consumer expenditure data by household income decile from the U.S. Bureau of Labor Statistics’ Consumer Expenditure Survey[7] and decile distributions of SNAP benefits as reported by the Congressional Budget Office,[8] we calculated sales tax liability per household income decile, first with unprepared foods (groceries) excluded from the sales tax, and then with them included along with a revenue-neutral rate reduction. Because foods purchased with SNAP benefits are exempt from sales tax in all states, we adjust the taxable base by the amount of SNAP benefits utilized by each decile.[9] We then used data on income per decile to calculate sales tax liability as well as effective taxation as a percentage of personal income by decile. Finally, we account for the sales taxation of business inputs, which is necessary for calculations of revenue-neutral rate reductions.

This approach allows us to test the common assumption that exempting groceries from the sales tax base is a progressive policy. We also used data on income ranges and household sizes to allow us to calculate the distributional effect of per-person grocery tax credits. Our approach is similar, but not identical, to that of Sheffrin and Johnson (2015), who likewise conclude that including groceries in the sales tax base with a corresponding adjustment in the overall tax base would represent a beneficial change.[10]

Although consumer expenditure data are available through calendar year 2020, we have elected to use 2019 data as more representative of ordinary consumption and income. We regard the economic dislocations of the early pandemic period as a distortion, albeit a significant and still lingering one, and are wary of basing our analysis on these anomalous consumption patterns. In the early days of the pandemic, for instance, with most restaurants closed or carryout-only, and most white-collar employees working remotely, high earners increased their grocery purchases to offset meals that otherwise would have been purchased at restaurants—not just at dinner, but also with the replacement of the downtown lunch trade with home-prepared midday meals. While our analysis, using pre-pandemic figures, shows that the grocery exemption lacks the progressive characteristics often ascribed to it, using pandemic-era data would overstate our case, and is avoided.[11]

We estimated sales tax liability for consumers in each income decile three times, under the following assumptions.

- Scenario 1: 6 percent sales tax rate with groceries excluded from the tax base

- Scenario 2: groceries restored to the tax base with the rate set at a revenue-neutral 5.48 percent

- Scenario 3: grocery tax paired with a $75 per-person grocery tax credit for households in the first seven income deciles, taxed at a revenue-neutral 5.75 percent rate

The lowest 20 percent of households sees sales tax relief in both scenarios which include groceries in the base, while middle earners see a modest increase in overall liability if groceries are taxed without an offset, but benefit—along with lower-income households—if grocery taxation is paired with a tax credit. In our scenarios, an income-capped $75 per person credit is sufficient to reduce liability for the first seven deciles. If the credit were uncapped (available to the top three deciles as well), it would have to be moderately larger to provide benefits to the deciles already covered, since the additional cost would lead to an adjustment in the revenue-neutral rate.

It would also be possible to adopt comprehensive tax reform that combines the taxation of groceries, the provision of grocery tax credits, and a commensurate reduction in income taxes rather than a revenue-neutral reduction in the sales tax rate. Such a package would shift more of the tax burden from income to sales taxes, even after accounting for the grocery tax credit against income tax liability, enhancing economic efficiency while addressing progressivity through sales tax changes.

The following table explores the sales tax liability implications by decile for all three scenarios, and indicates how much the changes from the Scenario 1 baseline represent as a percentage of after-tax income. For instance, under Scenario 3, where groceries are included in the sales tax base and the additional revenue generated by their inclusion is returned in the form of a $75 per person grocery tax credit and a reduction in the general sales tax rate, the lowest decile’s overall sales tax liability as a percentage of after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. falls more than two percentage points, from 7.51 to 5.19 percent of after-tax income.

It is important to note, of course, that for the lowest-income households, consumption considerably outstrips after-tax income, since much of these households’ consumption is financed by government transfers, including SNAP benefits. Since a household in the lowest decile pays relatively little sales tax on groceries even when they are included in the base (since SNAP purchases comprise a significant share of the grocery budget), the benefits of a lower overall rate on other purchases, plus the grocery credit, confer tax advantages that outweigh any additional liability on groceries purchased outside of SNAP.

| Sales Tax Liability and Change in Liability as a Percentage of Income by Decile Under Three Scenarios | ||||||

|---|---|---|---|---|---|---|

| Decile | Scenario 1 Liability | Income % | Scenario 2 Liability | Income % | Scenario 3 Liability | Income % |

| 1st | $480 | — | $438 | -0.65% | $331 | -1.68% |

| 2nd | $591 | — | $563 | -0.16% | $465 | -0.54% |

| 3rd | $698 | — | $749 | 0.18% | $633 | -0.41% |

| 4th | $861 | — | $973 | 0.30% | $854 | -0.32% |

| 5th | $970 | — | $1,078 | 0.23% | $955 | -0.26% |

| 6th | $1,127 | — | $1,238 | 0.19% | $1,117 | -0.20% |

| 7th | $1,295 | — | $1,419 | 0.17% | $1,287 | -0.18% |

| 8th | $1,478 | — | $1,608 | 0.14% | $1,688 | 0.09% |

| 9th | $1,881 | — | $2,034 | 0.13% | $2,135 | 0.08% |

| 10th | $2,748 | — | $2,875 | 0.06% | $3,018 | 0.06% |

| Rate | 6.00% | 5.48% | 5.75% | |||

| Sources: U.S. Bureau of Labor Statistics; U.S. Department of Agriculture; Congressional Budget Office; Tax Foundation calculations. | ||||||

We can also consider sales tax liability as a percentage of overall consumption for each decile under all three scenarios. With groceries excluded from the base, sales tax liability averages 1.93 percent of consumer expenditures for all taxpayers in aggregate, with very little variation—across all deciles, the range runs from 1.86 to 1.99 percent. Including groceries in the sales tax base reduces the effective rate on consumption for the lowest deciles, with an even larger improvement if paired with a credit.

| Decile | Scenario 1 | Scenario 2 | Scenario 3 |

|---|---|---|---|

| 1st | 1.86% | 1.70% | 1.28% |

| 2nd | 1.88% | 1.79% | 1.48% |

| 3rd | 1.88% | 2.02% | 1.70% |

| 4th | 1.96% | 2.22% | 1.95% |

| 5th | 1.96% | 2.18% | 1.93% |

| 6th | 1.99% | 2.18% | 1.97% |

| 7th | 1.95% | 2.14% | 1.94% |

| 8th | 1.95% | 2.12% | 2.22% |

| 9th | 1.94% | 2.10% | 2.20% |

| 10th | 1.88% | 1.97% | 2.07% |

| Source: Tax Foundation calculations. | |||

The Economic Case for Taxing Groceries

Sales taxes account for one-third of state tax revenue, but they are under pressure.[12] This is a troubling development, as consumption taxes have the advantage of providing greater revenue stability for governments while being more economically efficient for taxpayers.

Income can vary greatly from year to year, particularly capital gains income, which will track stock markets and other avenues of investment. While people adjust their consumption levels during economic downturns, consumption is considerably more fixed than, say, stock market performance. This reliable source of revenue is of considerable importance to governments, but it is undermined by decades of sales tax base-narrowing provisions, not only because they reduce overall sales tax reliance, but also because they create a less diversified, and typically more volatile, base. Excluding groceries from the sales tax shrinks the sales tax base by excluding a particularly stable share of it. Excluding groceries from the sales tax base in many states is one of the reasons why sales tax bases are 39 percent narrower than they were 20 years ago.[13]

Income taxes reduce the return to both labor and investment. They are a tax on both present and future consumption. Conversely, sales taxes only fall on present consumption, and thus do not have the same impact on economic decision-making that affects labor supply, capital investment, or productivity gains. All else being equal, heavier reliance on sales rather than income taxes is better for a state’s competitiveness and economic growth. Consequently, policies that undermine sales tax reliance are undesirable in themselves, and must be justified with appeal to some other desirable outcome. Typically, the competing goal is greater tax progressivity. But if grocery tax exemptions are self-defeating for that purpose, then policymakers are left with the efficiency losses without the countervailing equity gains.

Public perceptions regarding grocery taxation are not easily changed. In states where groceries are taxed, the policy is not always very controversial, because it is deemed the ordinary condition, at least until policymakers agitate for change. But in states where groceries are exempt, or taxed at a preferential rate, a reversal is likely to meet with stiff opposition unless the public can be convinced of the benefits. In Utah, what began as a broader tax reform package was ultimately condensed into a grocery taxation for income tax cuts swap, and lawmakers reversed their own decision in the face of a credible citizen effort to overturn the decision at the ballot. A more comprehensive approach, however, is possible, broadening the sales tax bases to include both groceries and consumer services (which tend to be consumed by higher earners) and is potentially paired with a modest grocery tax credit, with remaining revenues dedicated to income tax reductions. This approach can manage something of a tax policy hat trick: it is progressive, it yields greater revenue stability, and it makes the overall tax code more pro-growth.

Meanwhile, it has become popular, in states which currently tax groceries, for lawmakers to propose reductions or repeal. Lawmakers should understand that this change actually increases tax liability for the lowest-earning households compared to raising the same amount with a lower rate, while providing only extremely modest tax savings for the middle class, and does so against the backdrop of greater volatility and reduced economic competitiveness. The time has come for lawmakers to rethink the grocery tax exemption.

| Percentage of Each Consumer Expenditure Category and Relevant Subcategory Included in Base | |||

|---|---|---|---|

| Consumer Expenditure Category/Subcategory | Included Share | ||

| Food | 55% | ||

| Food at home | 9% | ||

| Cereals and bakery products | 0% | ||

| Meats, poultry, fish, and eggs | 0% | ||

| Dairy products | 0% | ||

| Fruits and vegetables | 0% | ||

| Other food at home | 23% | ||

| Food away from home | 100% | ||

| Alcoholic beverages | 100% | ||

| Housing and household goods/services | 17% | ||

| Shelter | 0% | ||

| Utilities, fuel, and public services | 20% | ||

| Utilities and fuels | 0% | ||

| Telephone services | 57% | ||

| Water and other public services | 0% | ||

| Household operations | 0% | ||

| Housekeeping supplies | 93% | ||

| Laundry and cleaning supplies | 100% | ||

| Other household products | 100% | ||

| Postage and stationery | 58% | ||

| Household furnishings and equipment | 100% | ||

| Apparel and services | 100% | ||

| Transportation | 50% | ||

| Vehicle purchases | 100% | ||

| Gasoline, other fuels, and motor oil | 0% | ||

| Other vehicle expenses | |||

| Vehicle finance charges | 0% | ||

| Maintenance and repairs | 50% | ||

| Vehicle rental, leases, licenses, etc. | 66% | ||

| Vehicle insurance | 0% | ||

| Public and other transportation | 0% | ||

| Health care | 0% | ||

| Entertainment | 100% | ||

| Fees and admissions | 100% | ||

| Audio and visual equipment and services | 100% | ||

| Pets, toys, hobbies, and playground equipment | 100% | ||

| Personal care products and services | 60% | ||

| Personal insurance and pensions | 0% | ||

| Miscellaneous | 48% | ||

| Sources: U.S. Bureau of Labor Statistics; Tax Foundation calculations. | |||

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe[1] Janelle Cammenga, “Facts & Figures 2022: How Does Your State Compare?” Tax Foundation, March 29, 2022, .

[2] See, by way of example, “Food Definition Issues,” Streamlined Sales Tax Project Discussion Paper, Jan. 20, 2005, https://www.streamlinedsalestax.org/docs/default-source/issue-papers/food.pdf?sfvrsn=8dead2fd_6.

[3] Wisconsin Department of Revenue, “Sales of Ice Cream Cakes and Similar Items,” Nov. 8, 2010, https://www.revenue.wi.gov/Pages/TaxPro/2010/news-2010-101108c.aspx.

[4] Tax Foundation, “Pumpkin Tax in Iowa is Gone,” Nov. 1, 2007, .

[5] Katherine Loughead, “Sales Taxes on Soda, Candy, and Other Groceries, 2018,” Tax Foundation, July 11, 2018, .

[6] The composition of the representative sales tax base can be found in Table 4 at the end of this paper.

[7] U.S. Bureau of Economic Statistics, Consumer Expenditure Survey Table 1110 (2019), https://www.bls.gov/cex/tables/calendar-year/mean-item-share-average-standard-error.htm, with detailed breakdown at https://www.bls.gov/cex/tables/calendar-year/mean/cu-all-detail-2019.pdf.

[8] Calculated and updated from Congressional Budget Office, “The Effects of Potential Cuts in SNAP Spending on Households with Different Amounts of Income,” March 16, 2015, https://www.cbo.gov/publication/49978.

[9] SNAP benefits can be used to purchase food, as well as to purchase plants and seeds intended to grow food for household consumption. Benefits cannot be used to purchase non-food items commonly available at grocery stores, including paper products, cosmetics, toiletries, pet foods, vitamins, and tobacco, nor can they be used for alcoholic beverages, foods consumed in the store, or any hot prepared foods, all of which are typically outside a grocery tax exemption. Our analysis does not adjust for the share of SNAP benefits used to purchase plants or seeds, as this is assumed to be trivial.

[10] Steven M. Sheffrin and Anna Johnson, “Rethinking the Sales Tax Food Exclusion with SNAP Benefits,” State Tax Notes, Jan. 11, 2016, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2597228.

[11] This is, of course, one of only several effects of the pandemic. Another effect is a decline in consumption of personal services (often untaxed) and a temporary shift to the purchase of more tangible goods (frequently taxed), which is also more significant for high earners.

[12] Jared Walczak, “State Sales Tax Breadth and Reliance, Fiscal Year 2020,” Feb. 9, 2021, https://taxfoundation.org/sales-tax-base-reliance-2020.

[13] Id.

Share this article